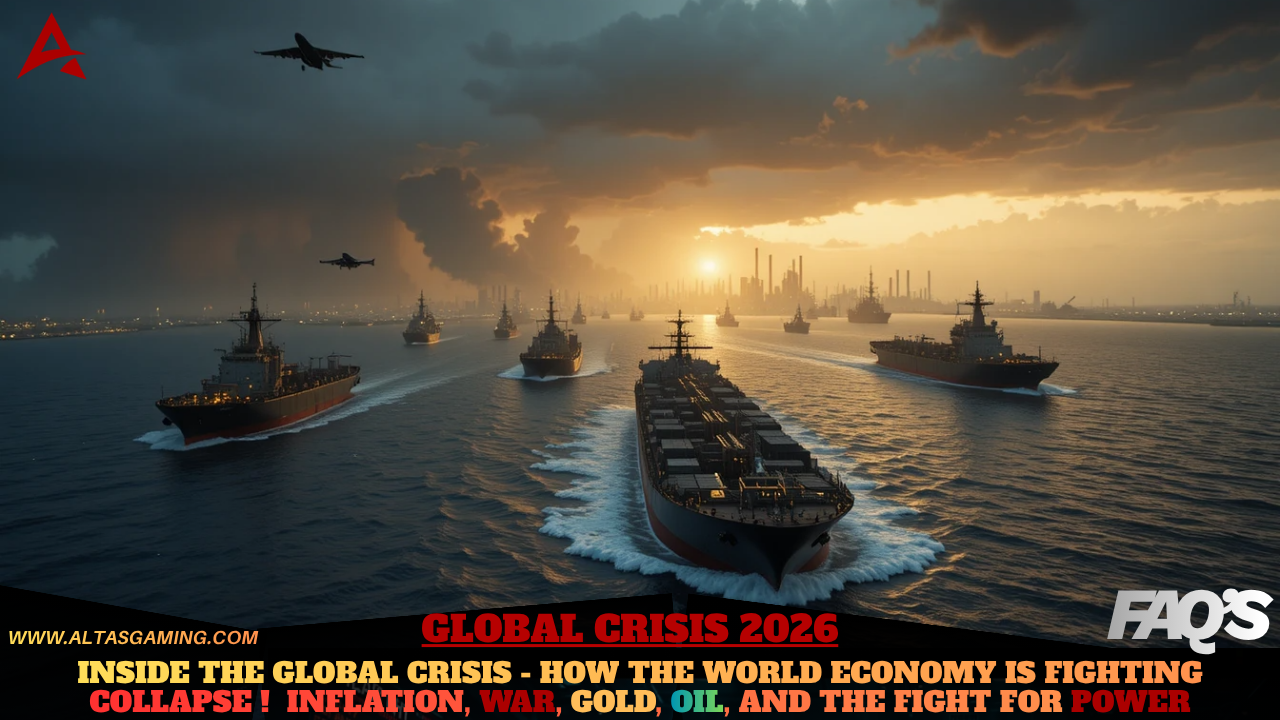

Global Crisis 2026 -Inside the Strait of Hormuz Crisis – The Shipping Route That Controls the World Economy

By Atlas Gaming Editorial – World Affairs & Global Economics Desk | May 2026

A complete analysis of the Strait of Hormuz crisis, global inflation, the war in the Middle East, rising gold prices, the BRICS challenge to the dollar, and how all of it is reshaping everyday life around the world.

Introduction – One Strait. The Entire World Economy.

There is a narrow strip of water, barely 21 miles wide at its narrowest point, nestled between the southern coast of Iran and the northern tip of Oman. It is called the Strait of Hormuz. For most people who have never studied geography or global trade, it barely registers. But in the spring of 2026, the disruption of that single waterway triggered what the head of the International Energy Agency called “the greatest global energy security challenge in history” and what analysts at Barclays, Goldman Sachs, and the Dallas Federal Reserve are describing as a potential economic crisis of generational proportions.

Until the US–Israeli war against Iran, the Strait of Hormuz was open and about 25% of the world’s seaborne oil trade and 20% of the world’s liquefied natural gas passed through it. Shipping traffic through the Strait of Hormuz has been largely blocked by Iran since February 28, 2026, when the United States and Israel launched an air war against Iran. In retaliation, Iran launched missile and drone attacks on Israel, US military bases, and US-allied Gulf states. The Iranian Revolutionary Guard Corps issued warnings forbidding passage through the strait, boarded and attacked merchant ships, and laid sea mines in the strait.

Ship transits dropped from around 130 per day in February to just 6 in March a collapse of about 95%. The disruption is hitting a large share of global oil and gas supplies, with immediate consequences for production, trade and consumption worldwide.

This article is the complete guide to understanding everything happening right now from the Strait of Hormuz crisis and its chain reactions across the global economy, to American inflation, gold prices, the war of currencies between the West and BRICS nations, and the hidden risks that most people still do not fully understand. Read it section by section. Share what matters.

Section 1 – What Is the Strait of Hormuz and Why Does It Control the World Economy?

The Strait of Hormuz is the single most strategically important body of water on the planet. It is the only maritime exit point for the oil and gas produced by Saudi Arabia, Iran, Iraq, Kuwait, Qatar, Bahrain, and the United Arab Emirates the nations that collectively possess the majority of the world’s proven oil reserves. Without the Strait of Hormuz, those reserves have no way of reaching the ships that carry them to refineries and markets across Asia, Europe, and beyond.

According to the US Energy Information Administration, around 20 million barrels per day of oil and petroleum liquids moved through the Strait of Hormuz in 2024, equivalent to about 20 percent of global petroleum liquids consumption. The IEA also reports that roughly 19 percent of global LNG trade depends on Hormuz. Disruption in Hormuz is not a regional oil story. It is a global inflation, shipping and growth story.

The crisis that erupted on February 28, 2026, when the United States and Israel launched Operation Epic Fury coordinated airstrikes on Iranian military facilities, nuclear sites, and leadership that resulted in the death of Supreme Leader Ali Khamenei immediately transformed the strait from a functioning global artery into a war zone. Iran’s response was to declare the strait closed to all hostile nations’ shipping, mine the waterway, and begin attacking vessels attempting to pass through.

Brent crude surged past $120 a barrel within weeks, reaching levels not seen since Russia’s invasion of Ukraine in 2022. Unlike previous disruptions caused by a supplier exiting the market, the 2026 crisis involves a strategic chokepoint effectively going dark. This is structurally different and, in many ways, far more difficult to compensate for. OPEC’s position shifted almost overnight the organization that spent much of 2025 managing a surplus now faces a shortfall it cannot fully fill.

The alternative pipeline routes that bypass the strait Saudi Arabia’s East-West Pipeline and Abu Dhabi’s Crude Oil Pipeline are meaningful but insufficient. The IEA estimates that only 3.5 to 5.5 million barrels per day can be redirected through Saudi and Emirati pipelines outside Hormuz. Beginning with a baseline of 20 million barrels per day, the implied net shortfall is roughly 14.5 to 16.5 million barrels per day.

The global consequence of this shortfall is not merely higher petrol prices at the pump. It cascades through every layer of the modern economy. Every product manufactured using petrochemicals, every food grown using fertilizer, every garment made from synthetic fabric, every vehicle assembled from aluminium, every package delivered by fuel-powered logistics all of it costs more when the Strait of Hormuz is closed.

Beyond energy, the conflict is disrupting key non-oil commodities methanol, aluminium, sulphur and graphite impacting global manufacturing and the green energy transition. Around a third of global seaborne methanol trade passes through the Strait of Hormuz. The Gulf is a significant supplier of high-grade iron ore pellets and direct-reduced iron premium feedstocks for global steelmaking. Shipowners began avoiding the strait almost immediately after the conflict escalated, making it more difficult to secure vessels and prompting buyers across Asia, India and the Middle East to pause new procurement.

The fertilizer consequences alone represent a threat to global food security. Roughly one-third of global fertilizer trade transits the Strait of Hormuz, including large volumes of nitrogen exports. New Orleans fertilizer hub urea prices have already risen from $475 per metric ton to $680 per metric ton. If those shipments are blocked during the spring planting season, it could wreak havoc on food inflation.

Section 2 – Why Is the United States Selling Gold and What Steps Is It Taking to Stabilise Its Economy?

The gold market in 2025 and 2026 became one of the clearest indicators of how much trust investors had left in the stability of traditional financial systems and the answer was: not much.

Gold prices soared in 2025, driven by tariff uncertainty and strong demand from ETFs and central banks, climbing as much as 55% and surpassing $4,000 per ounce for the first time in October. J.P. Morgan Global Research forecasts ongoing robust investor demand for gold, with prices expected to push toward $5,000 per ounce by the fourth quarter of 2026, with $6,000 per ounce a possibility longer term. Central bank and investor demand for gold is set to remain strong, averaging 585 tonnes a quarter in 2026.

The United States itself holds approximately 81% of its total foreign reserves in gold making it the world’s largest national gold holder. The question of why gold is becoming so central to the global economic story in 2026 comes down to three converging pressures: Trump’s tariff policies, the Iran war’s energy shock, and the broader crisis of confidence in dollar-denominated assets that these events have combined to produce.

When governments and central banks sell gold, they typically do so for one of two reasons: to raise emergency liquidity, or to intervene in currency markets. In the current environment, multiple nations facing energy-price-driven fiscal pressure have had to liquidate reserves to fund subsidies and stabilise currencies. The United States Treasury, meanwhile, has been navigating the extraordinary combination of record tariff revenues the United States collected $187 billion more in tariff revenue in 2025 than in 2024, a nearly 200% increase alongside stubborn inflation that the Federal Reserve is struggling to control without triggering a recession.

The Federal Reserve’s dilemma is acute. Raising interest rates further to combat inflation risks slowing an already fragile economy and pushing unemployment higher. Cutting rates risks reigniting the inflation the Fed spent years trying to suppress. The Hormuz energy shock has made this choice essentially impossible in the near term higher energy prices are inflationary by definition and are largely outside the Fed’s ability to control through monetary policy.

Section 3 – How Far Has Inflation Risen in America Due to Trump’s Policies?

The story of American inflation in 2025 and 2026 is a story in two acts. The first act was the tariff-driven inflation of 2025 that was worse than most economists predicted but not as catastrophic as the most alarming forecasts. The second act now underway is the energy shock from the Iran war being layered on top of an economy already strained by trade policy uncertainty.

Goldman Sachs economists estimated that tariffs caused inflation to increase by half a percentage point in 2025 — roughly in line with Federal Reserve Chair Jerome Powell’s statement that Trump‘s tariffs were responsible for the entirety of inflation’s rise above the central bank’s 2% annual inflation target, which ended the year at 2.7%. Goldman anticipates inflation will increase by three-tenths of a percentage point in just the first six months of 2026.

Although businesses footed roughly 80% of the tariff bill in 2025, they are now starting to pass those costs along to customers. Items with low profit margins, including groceries, are among the first to rise. A looming spike in prices sets up a tricky decision for Trump ahead of the midterm elections: stay the course on tariffs or ease up to give some relief to Americans struggling with the high cost of living.

Then came the Iran war. While many economists predicted at the beginning of 2026 that tariff-related headwinds would begin to relent, the Iran war threw a wrench in those plans. Inflation is now trending upward as a result of the energy shock stemming from the war. Job growth is stagnating, developing a noxious combination of higher inflation and slow growth. That combination has some economists whispering the dreaded S-word: stagflation a brutal combination of stagnating growth and persistent inflation.

J.P. Morgan now sees a 0.2 percentage point hit to U.S. GDP, which moves its estimate for 2026 down to 1.3%. Core PCE inflation is forecast to increase to 3.1%. “The worsening growth and inflation outcomes leave the Fed with a challenging dilemma,” the institution noted.

For ordinary Americans, the concrete impact is felt across multiple spending categories simultaneously. Car prices could rise by as much as 11.4% under some scenarios due to auto tariffs. Grocery prices face upward pressure from both fertilizer cost spikes and fuel surcharges passed through distribution chains. Housing affordability has not recovered from the previous rate cycle. Higher energy costs are set to drive up delivery packages, airfares, and food prices in the coming months, and a Goldman Sachs note gives it to July until the US starts to run out of jet fuel, meaning airlines would likely dramatically cut back on flights.

Section 4 – Are People in the United States Protesting Against Economic Pressure and Government Policies?

The political and social pressures building within the United States in 2026 reflect the cumulative weight of three years of economic strain. While large-scale street protests specifically organised around inflation have been less visible than in some other democratic countries, the political discontent is real, measurable, and consequential.

Public approval ratings for economic management have declined sharply across 2025 and into 2026. The combination of tariff-driven price increases that disproportionately affect working and middle-class households who spend a higher proportion of their income on goods than wealthy households and an energy shock that is pushing fuel, food, and transport costs higher simultaneously has generated widespread frustration.

The political dimension is acute as the United States approaches midterm elections. A looming spike in prices sets up a tricky decision for Trump ahead of the midterms: stay the course on tariffs or ease up to give some relief to Americans who are struggling with the high cost of living. Consumer confidence surveys and economic sentiment indexes show Americans are deeply concerned about the direction of the economy. Labour movements have been increasingly vocal about real wage erosion the phenomenon where nominal wages rise but purchasing power falls because prices are rising faster.

The Iran war has added a new dimension to domestic discontent. Critics from across the political spectrum have raised questions about the cost and strategic rationale of military engagement at a moment when the domestic economy is already under stress. The human cost of the conflict casualties at US military bases in the Gulf including Bahrain, the UAE, and Qatar has generated both grief and political anger.

Section 5 – What Could Happen Next to the U.S. Economy If Inflation and Political Tensions Continue?

The range of scenarios for the US economy from mid-2026 onward is unusually wide, reflecting genuine uncertainty among professional forecasters about how the multiple simultaneous shocks tariffs, energy prices, war costs, and Federal Reserve constraint will resolve.

Moody’s recession odds hit 49% in March 2026. Goldman Sachs forecasts a 30% risk of recession and EY-Parthenon has the odds at 40%. Moody’s economist Mark Zandi stated that while the US should avoid a recession, he expects the economy to further diminish even if the war concludes in the next few weeks. “The economy should avoid a recession, but growth will fall well short of potential, jobs will remain largely flat, and unemployment will drift higher,” he said.

Federal Reserve Bank of Dallas research estimates that a closure of the Strait of Hormuz that removes close to 20 percent of global oil supplies during the second quarter of 2026 is expected to raise the average West Texas Intermediate oil price to $98 per barrel and lower global real GDP growth by an annualised 2.9 percentage points.

The worst-case scenario economic analysts discuss is a prolonged stagflationary period slower growth combined with persistent elevated inflation that forces the Federal Reserve to choose between fighting inflation (by keeping rates high, slowing growth further) and supporting employment (by cutting rates, risking re-accelerating inflation). This is the same trap the Fed fell into in the late 1970s, and escaping it then required interest rates above 20%, a severe recession, and years of economic pain. Most analysts believe the current Federal Reserve would not allow that scenario to develop fully but the conditions that enable it are closer to present than they have been in four decades.

Section 6 – What Are Israel’s Strategic Plans in the Middle East?

Operation Epic Fury the joint US-Israeli air campaign launched on February 28, 2026, that killed Ali Khamenei and targeted Iran’s nuclear programme and military infrastructure represents the most significant Israeli military action in decades and one whose strategic consequences will unfold over years, not months.

Israel’s stated strategic objective was to permanently eliminate Iran’s nuclear weapons programme. Whether that objective has been achieved remains genuinely uncertain intelligence assessments are divided on how much of Iran’s nuclear capability was destroyed versus dispersed or hidden in advance. The assassination of Khamenei and the subsequent power struggle within Iran’s political system created a period of Iranian internal instability that may or may not produce a more pragmatic successor regime.

Israel’s broader strategic calculation in the Middle East has always been organised around a single core concern: preventing any regional power from acquiring nuclear weapons. With that immediate objective addressed at least in the near term Israeli strategic attention is expected to refocus on consolidating its regional position, managing the consequences of Hezbollah’s ongoing rocket fire from Lebanon (which Israeli counterstrikes have dramatically degraded but not eliminated), and navigating the diplomatic fallout from an operation that, while supported by the United States, has drawn significant international criticism.

The longer-term strategic question for Israel is what kind of Iran emerges from the current crisis. A weakened but resentful Iran that reconstitutes its nuclear programme within a decade is a different strategic problem from an Iran whose political system has been destabilised enough to produce meaningful internal reform. Israeli intelligence estimates of these outcomes vary widely, and the honest answer is that nobody knows.

Section 7 – What Are Russia, China, and Iran Planning Together?

The alignment of Russia, China, and Iran as strategic partners has deepened significantly since Russia’s 2022 full-scale invasion of Ukraine, and the 2026 Iran war has accelerated that deepening further. Understanding what these three powers are planning together requires separating what is known from what is speculated.

What is known: Russia and China have been systematically building financial infrastructure that bypasses Western-controlled systems- SWIFT for payments, the dollar for trade settlement for several years. Russia and China now settle around 90% of their bilateral trade in rubles and yuan. China’s Cross-Border Interbank Payment System (CIPS) processed the equivalent of $245 trillion in yuan-denominated transactions in 2025, providing real, operational infrastructure as a settlement alternative to dollar-denominated SWIFT channels.

Iran, despite the devastating impact of the US-Israeli strikes on its military and economic infrastructure, retains enormous strategic value for both Russia and China as a source of oil, as a geographic buffer against Western power projection into Central Asia, and as a demonstration case for what happens to nations that accept Western-imposed isolation. China is Iran’s primary oil customer the two have maintained significant energy trade throughout the conflict and Russia has been providing Iran with military equipment and diplomatic cover within the UN Security Council.

The three nations share a common strategic interest that goes beyond any specific alliance: the gradual erosion of the institutional architecture through which the United States projects global power the dollar’s reserve currency status, the SWIFT financial system, the NATO alliance structure, and the network of US military bases that encircle the Eurasian landmass. None of them expects to achieve this through direct military confrontation with the United States. All of them are investing heavily in the parallel systems that make such confrontation less necessary over time.

Section 8 – Which Countries Are Being Most Affected Right Now?

The countries suffering most acutely from the combined impact of the Hormuz crisis, global inflation, and supply chain disruption fall into several distinct categories.

Energy-importing developing nations face the most immediate and severe crisis. Countries across South and Southeast Asia India, Pakistan, Bangladesh, Sri Lanka, Vietnam, the Philippines, Thailand, and Indonesia import a substantial proportion of their energy needs from the Persian Gulf. Rising oil prices represent not merely a transport cost increase but a direct hit to agricultural productivity (fertilizer), manufacturing competitiveness, and fiscal stability. Pakistan and Sri Lanka, which were already managing post-2022 debt crises, face renewed pressure on their currencies and foreign exchange reserves.

European nations are experiencing what analysts are calling a second energy crisis, the first having been triggered by Russia’s 2022 Ukraine invasion. The war has precipitated a second major energy crisis for Europe, primarily through the suspension of Qatari liquefied natural gas and the closure of the Strait of Hormuz. The conflict coincided with historically low European gas storage levels estimated at just 30% capacity following a harsh 2025-2026 winter causing Dutch TTF gas benchmarks to nearly double to over €60/MWh by mid-March. The European Central Bank postponed its planned interest rate reductions, raising its 2026 inflation forecast. UK inflation is expected to breach 5% in 2026.

Japan and South Korea are among the most acutely vulnerable major economies, deriving the vast majority of their oil from Gulf suppliers. Japanese refiners obtain about 95% of their crude oil from Saudi Arabia, Kuwait, the United Arab Emirates, and Qatar. About 70% of this Middle Eastern oil is delivered to Japan by ships that pass through the Strait of Hormuz.

Iran itself faces economic catastrophe. From March 2025 to March 2026, the price of bread and cereals increased by 140%, red meat and poultry by 135%, oil and fats by 219%, fruits and nuts by 104.2%, and dairy products by 116.8%. The war has destroyed critical infrastructure, caused widespread layoffs, and triggered internet blackouts that have cut millions of Iranians off from digital economic activity.

Gulf states face a paradox: they are the world’s largest energy exporters but their export revenue has been effectively zeroed by the strait closure. Iraq and Kuwait began curtailing oil production in early March 2026 because their storage capacity was filling up with oil they could not ship.

Section 9 – How Are Shipping Routes and Maritime Tensions Affecting the Global Economy?

The Strait of Hormuz crisis sits within a broader pattern of maritime disruption that has been building since the Houthi attacks on Red Sea shipping began in late 2023. The Red Sea which carries roughly 12% of global trade including significant container shipping between Asia and Europe through the Suez Canal was already severely disrupted before the Hormuz crisis began. The combination of both routes under pressure simultaneously represents an unprecedented dual shock to global maritime trade.

Global merchandise trade is expected to slow sharply, from about 4.7% growth in 2025 to 1.5–2.5% in 2026. Energy shocks are pushing up prices and increasing the cost of living. Investors are pulling back from developing countries, weakening currencies and raising borrowing costs. 3.4 billion people live in countries already spending more on debt than on health or education.

Major global maritime shipping companies Maersk and Hapag-Lloyd have already suspended Mideast routes. If Strait of Hormuz disruptions force vessel rerouting, inland port disruption can escalate quickly. The initial ocean impact may take 10–14 days to appear, but the real pressure typically hits within 2–5 weeks as diverted containers arrive in clusters, terminal congestion rises, and drayage demand outpaces truck and chassis availability. Disrupted trade lanes also reduce empty container availability, tightening export capacity in other markets, including North America. That can lead to missed appointments, higher demurrage charges, and severe congestion at already strained ports.

The insurance dimension of the crisis deserves particular attention. War risk insurance premiums for vessels attempting to enter the Persian Gulf have risen to levels that effectively make commercial shipping economically nonviable even for operators willing to accept physical risk. Protection and indemnity insurance is critical for shipping. War risk coverage was removed for vessels in the strait, making the economic risk too high for ship owners to use the waterway.

Section 10 – Which Countries Face Severe Economic Collapse or Near-Shutdown?

Several nations were already on the brink of economic crisis before the Hormuz disruption began. The energy shock has accelerated their descent.

Lebanon entered 2026 already having experienced one of the worst economic collapses in modern history, with its currency having lost more than 95% of its value since 2019. The regional conflict has added military damage to fiscal catastrophe, and the country’s ability to import basic goods all of which require foreign currency it does not have is critically compromised.

Sri Lanka completed a debt restructuring in 2024 after its 2022 default but remains extraordinarily vulnerable to commodity price shocks. Higher oil prices represent an immediate fiscal crisis for an economy still rebuilding reserve buffers.

Pakistan carries one of the highest debt service-to-revenue ratios in the world and has been through multiple IMF bailout programs. Higher energy import costs combined with a weakening currency and rising domestic food prices are creating conditions for renewed fiscal instability.

Egypt carries enormous external debt and has been managing a severe foreign exchange shortage. The Suez Canal its primary source of foreign exchange revenue has seen dramatically reduced traffic since the Red Sea crisis began, compounding fiscal pressure at the worst possible time.

Argentina remains in chronic crisis regardless of external shocks. The combination of its domestic structural problems and external commodity price volatility continues to test the limits of its ongoing reform programme.

Many developing countries already face high debt service burdens, limited fiscal space and constrained access to finance. These socio-economic implications are being compounded by the Hormuz disruption, which is raising costs for the most vulnerable populations.

Section 11 – Is the World Moving Toward a New Global Recession or Economic Depression?

The honest answer is that as of mid-2026, the world is closer to a global recession than at any point since the COVID-19 pandemic and the combination of factors currently in play could, in a worst-case scenario, produce something worse.

Global growth is expected to slow from 2.9% in 2025 to 2.6% in 2026, assuming the conflict does not intensify further. Rising geopolitical tensions are increasing uncertainty, making economic outcomes harder to predict and further weighing on investment and trade. The conflict is adding to already high global geopolitical risks, amplifying its effects beyond energy markets. Shipping and insurance costs are rising together, compounding the pressure. Inflation is picking up at the same time, adding to financial instability.

A recession is technically defined as two consecutive quarters of negative GDP growth. A depression is a sustained and severe decline in economic activity across multiple sectors and countries. The world is not currently in either, but the margin between the current trajectory and recessionary conditions has narrowed significantly. The key variables are: how long the Strait of Hormuz remains effectively closed, whether the Iran war expands to involve other regional actors, and whether central banks particularly the US Federal Reserve are able to manage the stagflationary dynamic without triggering a hard landing.

The 1970s stagflation episode is the most cited historical precedent for current conditions. In that period, an oil shock triggered by the 1973 Yom Kippur War and the 1979 Iranian Revolution produced a decade of slow growth, high inflation, and economic frustration across the Western world. The current shock is structurally larger the Hormuz closure removes approximately 20% of global oil supply from the market, compared to the roughly 4-7% removed during the 1973 embargo.

Section 12 – Why Are Gold and Oil Prices at the Centre of Global Tensions?

Gold and oil are not merely commodities. They are the two most politically loaded resources in the world and their prices in 2026 tell the story of everything happening simultaneously in the global economy.

Oil prices are the direct transmission mechanism for geopolitical instability into everyday life. When a conflict disrupts oil supply, every country in the world feels it within weeks in fuel bills, in food prices, in transport costs, in manufacturing costs, in inflation statistics, and ultimately in political outcomes. The Hormuz crisis has demonstrated once again that no amount of financial engineering or monetary policy can insulate national economies from a genuine large-scale disruption of physical oil supply.

Gold has climbed to record highs, with investors viewing it as a safe haven during times of uncertainty. Unlike money, which can drop in value due to inflation or overprinting, gold tends to retain its worth over time because it is a scarce resource. Fears that Trump’s tariffs, along with tax cuts and deregulation, will reignite inflation and force the US Federal Reserve to keep interest rates elevated have supported gold demand.

The simultaneous rise in both gold and oil tells a specific story: it is not merely that one commodity is scarce. It is that confidence in the stability of the entire financial and geopolitical order is eroding. When both gold and oil are rising strongly at the same time, markets are signalling a generalised fear not just of inflation, but of systemic instability. That fear is not irrational in mid-2026. It is a rational assessment of a world where the most important shipping route in existence is effectively closed, where the world’s largest economy is running tariff-driven inflation while engaging in a Middle Eastern war, and where the financial architecture that has governed global trade since 1944 is being actively challenged.

Section 13 – How Are Wars in the Middle East, Ukraine, and Asia Affecting Everyday Life?

For most people, wars are experienced not through military briefings but through price tags. The cascading economic effects of the simultaneous conflicts in the Middle East and the ongoing Russia-Ukraine war are felt in supermarkets, fuel stations, housing markets, and employment statistics around the world.

The food price impact is particularly stark and particularly unequal. The UN World Food Programme and various analysts warn that disruptions to fertilizer supply are driving long-term increases in global food prices, threatening a scenario similar to the 2022 food crisis. Roughly 50% of global urea and sulfur exports, along with 20% of global LNG a feedstock for nitrogen fertilizers transit the Strait of Hormuz.

For a family in Pakistan or Bangladesh spending 60–70% of its income on food, a 30–40% increase in staple food prices is not an inconvenience. It is a survival crisis. For a family in Germany or France spending perhaps 15% of income on food, the same percentage increase is painful and politically significant but not existential. The distributional impact of global commodity crises is one of the most important and least-discussed dimensions of geopolitical conflict.

The Ukraine war continues in its fourth year, with the front lines having shifted but the fundamental conflict unresolved. The war has permanently restructured European energy markets the continent that was significantly dependent on Russian gas has been forced to diversify its energy supply, at enormous cost and with incomplete success. The Hormuz crisis has compounded that challenge by removing LNG supplies that European buyers had come to depend on as a Russian substitute.

In Asia, the Taiwan Strait remains one of the world’s most closely watched potential flashpoints. The diversion of US military attention and resources to the Iran conflict has raised questions in Taipei and in Beijing about the credibility of American security commitments in the Pacific.

Section 14 – Could Global Shipping Routes Trigger a Worldwide Economic Crisis?

The world’s maritime shipping system operates through a small number of critical chokepoints narrow passages through which the vast majority of global seaborne trade must pass. The Strait of Hormuz is the most important. The Suez Canal and the associated Bab-el-Mandeb Strait linking the Red Sea to the Indian Ocean is the second. The Strait of Malacca, through which most Asia-Pacific trade flows, is the third. The Panama Canal is the fourth.

The simultaneous disruption of Hormuz and the Red Sea route both effectively compromised in early 2026 represents a scenario that global shipping and insurance industries had modelled as a severe stress test but had not actually experienced before. Ships rerouting around the Cape of Good Hope from Asia to Europe add approximately 10–14 days and substantial additional fuel costs to each voyage. Ships unable to access Gulf oil for cargo have no alternative of equivalent scale.

UNCTAD warns that these disruptions underscore the vulnerability of critical maritime chokepoints to geopolitical tensions and their potential to transmit shocks across supply chains and commodity markets. Economic impacts, both globally and for the region, will depend on the duration, intensity and geographic scope of the tensions.

The critical threshold analysts watch is duration. A one-quarter disruption of Hormuz is an oil and commodity shock painful but survivable. A two to three-quarter disruption becomes an inflation and growth shock with recession implications. A disruption lasting beyond one year would represent a structural transformation of global energy markets requiring the physical construction of new pipeline routes, the development of new suppliers, and a decade of investment in alternative supply chains all of which takes time that economies under acute pressure do not have.

Section 15 – Which Nations Are Secretly Preparing for Major Economic or Military Changes?

The honest answer is that almost every major nation is currently engaged in some form of strategic repositioning that it is not fully advertising publicly. The post-1945 international order the system of multilateral institutions, treaty relationships, and financial architecture built after World War II is under more simultaneous pressure than at any point since its creation.

Saudi Arabia is one of the most interesting cases. As both a founding member of the OPEC+ oil production bloc and a new member of BRICS, the Kingdom is simultaneously deepening its relationship with China (which has become its largest oil customer) and maintaining its security relationship with the United States. This dual position gives Riyadh unusual leverage in both directions but also makes it unusually vulnerable to the deterioration of US-China relations. The kingdom has been quietly building reserve buffers and diversifying its economic base through Vision 2030 precisely in anticipation of a world where oil revenue alone may not guarantee stability.

Turkey has positioned itself as a neutral transit hub for both East-West trade and East-West diplomacy maintaining relationships with both NATO allies and Russia, both Israel and Iran’s opponents. Some countries, such as Turkey, could seize this opportunity to establish themselves as hubs for international trade as traditional routes are disrupted.

India broke ranks with its BRICS peers in February 2026 to sign a trade deal with the United States, agreeing to halt purchases of Russian oil in exchange for reduced tariffs. This move signals New Delhi’s assessment that alignment with Western economic power remains more valuable than BRICS solidarity at least at this stage of the de-dollarisation experiment.

Section 16 – Is the Global Financial System Becoming Unstable and What Could Replace the Dollar?

The US dollar’s position as the world’s reserve currency the currency in which most international trade is priced and most central bank reserves are held is under the most sustained and organised challenge since the dollar displaced the British pound after World War II.

According to the Atlantic Council, as of November 2025, the US dollar is used in approximately 89% of currency exchanges and 56% of all foreign currency reserves held by central banks. The US Treasury market remains the world’s deepest and most liquid sovereign debt market.

These numbers represent continued dominance. But the direction of travel matters as much as the current position, and the direction has been toward gradual diversification away from dollar dependency for several years.

The BRICS Unit was launched in 2026 after a pilot program began on October 31, 2025 -100 Units supported by 40% gold and 60% BRICS currencies. Russia and China now settle around 90% of their bilateral trade in rubles and yuan. BRICS CBDC interoperability connecting Russia’s digital ruble, China’s digital yuan, and India’s digital rupee is one of the priorities of the BRICS de-dollarization plan in 2026.

The BRICS bloc, which now includes Brazil, Russia, India, China, South Africa, Saudi Arabia, the UAE, Iran, Egypt, Ethiopia, and Indonesia, represents roughly 45% of the world’s population and over 35% of global GDP by purchasing power parity. The bloc’s strategy is pragmatic, not revolutionary: build enough parallel infrastructure that the dollar becomes one settlement option among several, rather than the only viable choice.

However, the limitations of de-dollarisation are equally real. The yuan faces fundamental constraints: China maintains capital controls that limit free convertibility, and foreign investors cannot freely move capital in and out of Chinese markets. No alternative currency matches the dollar’s liquidity, the depth of US capital markets, or the legal and institutional trust underpinning dollar-denominated assets. The full replacement of the dollar as the global reserve currency, if it happens at all, is a decades-long process not an event.

Section 17 – How Are China, Russia, and BRICS Countries Challenging Western Economic Power?

The challenge to Western economic power being mounted by China, Russia, and the broader BRICS alignment operates on four simultaneous dimensions: financial infrastructure, trade currency diversification, commodity pricing power, and development finance.

On financial infrastructure, the BRICS Pay expansion has engineered connections across multiple essential national networks such as Russia’s SPFS, China’s CIPS, and India’s UPI. Systems like mBridge enable instant payments between central banks in China, Hong Kong, Thailand, and the United Arab Emirates using digital national currencies.

On trade currency diversification, the practical progress is real but uneven. Russia and China have achieved near-complete bilateral trade in non-dollar currencies, but India’s external affairs minister has explicitly stated that India has no policy to replace the dollar as the global reserve currency, reflecting the bloc’s internal divisions.

On commodity pricing, the addition of Saudi Arabia and the UAE to BRICS gives the bloc direct influence over OPEC dynamics the organisation that sets global oil production targets. If BRICS members begin pricing oil in non-dollar currencies to a significant degree, it would represent the most fundamental challenge to dollar dominance since the petrodollar system was established in the early 1970s.

Central banks have been aggressively diversifying into gold. The World Gold Council reports that central banks purchased more than 1,000 tonnes of gold annually for three consecutive years, more than double the 473-tonne annual average from 2010 to 2021. China shifted its foreign exchange reserves from 40% USD Treasury holdings around 2010 to less than 1% by 2025.

Section 18 – What Are the Biggest Hidden Global Risks That Most People Don’t Understand?

The risks that receive the least public attention are often more dangerous precisely because of their obscurity. Here are the hidden risks that analysts and institutions are watching most closely in 2026.

The fertilizer-food crisis time lag. The disruption to global fertilizer supply from the Hormuz closure will not show up immediately in global food prices it will appear in the 2026–2027 harvest cycle, when crops planted with insufficient or unaffordable fertilizer produce lower yields. The 2022 food crisis triggered by the Ukraine war took 12–18 months to fully manifest in food security statistics. The current disruption may be worse.

The pharmaceutical supply chain. The Strait of Hormuz carries significant volumes of pharmaceutical precursor chemicals, active pharmaceutical ingredients, and medical supplies. Petrochemical inputs, plastics, rubber, electronics, batteries, pharmaceuticals, and sugar are among the inputs at risk from Strait disruptions. A shortage of pharmaceutical precursors would take months to appear in actual drug supply chains but could affect the availability and price of medications across multiple disease categories.

The helium supply for semiconductors. The crisis has constrained the supply of helium, crucial for semiconductor manufacturing. The modern economy’s dependence on semiconductor chips is total from smartphones to cars to medical equipment to military systems and any constraint on helium, which is used in chip fabrication processes, represents a threat to every technology-dependent industry.

Developing country debt spirals. Higher interest rates, weaker currencies, and higher import costs are creating conditions for sovereign debt crises across multiple developing nations simultaneously. Individual debt crises are manageable; a wave of simultaneous defaults by multiple developing economies would overwhelm the IMF’s capacity to respond and could create contagion effects reaching developed financial markets.

The SWIFT sanctions paradox. The more aggressively Western nations use financial sanctions as a geopolitical tool, the more aggressively non-Western nations build alternatives to dollar-denominated systems. Each major sanctions episode – Russia in 2022, Iran ongoing accelerates the very de-dollarisation that US policymakers say they want to prevent.

Section 19 – Which Countries Could Become the Next Major Crisis Zones?

Beyond the current hot spots, several nations are watching their conditions deteriorate in ways that suggest they could become the next focal points of global economic or political crisis.

Bangladesh faces a dangerous combination of political instability following 2024’s political transition, dependence on Gulf remittances from workers whose employment is now disrupted by the Iran war, and a garment export industry facing input cost increases from petrochemical supply disruptions. The Asian garment industry, which relies on petrochemicals shipped through the Strait to produce synthetic fabrics, faces particularly acute risks.

Ethiopia – a new BRICS member is managing post-civil war reconstruction alongside drought impacts and a debt restructuring. Its alignment with BRICS represents both a genuine strategic choice and a signal of how many developing nations no longer feel they have meaningful access to Western-led development finance on acceptable terms.

Venezuela sits on the world’s largest proven oil reserves but cannot monetise them effectively due to US sanctions and infrastructure deterioration. A sustained period of high oil prices creates both opportunity and risk: higher global prices improve Venezuela’s theoretical revenue, but its inability to actually export at scale means the benefit is limited.

Tunisia has been experiencing a slow-motion political and economic deterioration since 2021. Higher food prices a direct consequence of global commodity disruptions could push an already stressed population beyond the tolerance threshold that triggered the 2011 Arab Spring in the first place.

Myanmar continues its civil war with no resolution in sight, affecting regional stability and supply chains in Southeast Asia.

Section 20 – How Are Rising Fuel, Food, Housing, and Transportation Costs Changing Life Around the World?

The cumulative impact of the multiple simultaneous economic shocks of 2025–2026 on everyday life varies dramatically by geography and income level, but the direction of change is consistent everywhere: the cost of living is rising faster than incomes in almost every country in the world.

In wealthier nations, the primary manifestation is the squeeze on discretionary spending. Households that could previously afford holidays, dining out, and consumer electronics are cutting back. Housing markets in cities from London to Sydney to Toronto have become inaccessible to all but the already-wealthy. The political consequence is a persistent cross-ideological anger at economic elites and institutions that seems to be intensifying rather than abating.

In middle-income nations, the consequences are more acute. A family in Turkey, Brazil, or South Africa faces the triple pressure of currency depreciation (which raises the cost of all imported goods), global commodity price inflation, and domestic interest rates raised to defend currencies that are themselves under pressure. Real wages in these countries have been declining in purchasing power terms for most of the period since 2022.

In low-income nations, the consequences are existential. Many developing countries already face high debt service burdens, limited fiscal space and constrained access to finance. Higher energy, fertilizer and transport costs may increase food costs and intensify cost-of-living pressures, particularly for the most vulnerable. The World Food Programme has warned of conditions that could produce a food security crisis comparable to or worse than 2022.

The transportation dimension is particularly consequential for globalised supply chains. The price of transportation has increased by 67.5% in Iran alone. Fuel surcharges are being applied across air cargo, sea freight, and road haulage simultaneously meaning that virtually every physical good that moves from producer to consumer costs more to move today than it did a year ago.

Housing, the largest single expenditure for most households in the developed world, remains at historically unaffordable levels in most major cities. The combination of the post-pandemic construction cost surge (driven by material and labour inflation), high interest rates, and now renewed energy cost pressures on both construction and household utility bills has produced a housing affordability crisis that shows no near-term path to resolution.

tlas Gaming Geopolitics Verdict

tlas Gaming Geopolitics Verdict

If there is a single lesson that the events of 2025–2026 are teaching with brutal clarity, it is this: the global economy is far more fragile, and far more interconnected, than most people understood when everything was working normally.

The Strait of Hormuz crisis is not an isolated event. It is the product of decades of geopolitical choices the decision to build global energy infrastructure around Gulf oil rather than diversify more aggressively, the decision to use financial sanctions as a primary foreign policy tool in ways that accelerated non-Western financial independence, the decision to allow global food supply chains to become dependent on fertilizer routes that pass through conflict zones. These are structural vulnerabilities, not accidents.

The BRICS de-dollarisation challenge is real but not imminent in its most dramatic form. The dollar’s dominance rests on institutional trust, market depth, and legal architecture that cannot be replicated quickly. But the direction of travel toward a more multipolar global financial system in which the dollar is one important currency among several rather than the singular reserve seems increasingly irreversible regardless of how the current crisis resolves.

What the Atlas editorial team believes people most need to understand is the time lag problem. Many of the consequences of what is happening in the spring of 2026 will not fully manifest until 2027 and beyond in food prices, in sovereign debt crises, in supply chain restructuring, in geopolitical realignments. The world is not at the peak of this crisis. It is somewhere in the middle of it. The decisions made by governments, central banks, and international institutions in the next twelve months will determine whether the eventual outcome is a painful but survivable adjustment or something considerably worse.

Frequently Asked Questions

What is the Strait of Hormuz and why does its closure matter so much? The Strait of Hormuz is a 21-mile-wide waterway between Iran and Oman that is the only maritime exit for oil and gas from Saudi Arabia, Iraq, Iran, Kuwait, Qatar, the UAE, and Bahrain. Approximately 20 million barrels of oil and 19% of global LNG transit it daily. Its effective closure since late February 2026 has removed roughly 20% of global oil supply from the market the largest such disruption in the history of the global oil market causing oil prices to surge above $120 per barrel, driving inflation higher across every country that imports energy, and disrupting supply chains for fertilizer, chemicals, metals, and dozens of other commodities.

How much has inflation risen in the United States because of Trump’s tariffs? Goldman Sachs estimated that Trump’s tariffs caused inflation to increase by approximately half a percentage point in 2025, pushing CPI inflation to 2.7% by year end above the Federal Reserve’s 2% target. Core PCE inflation is forecast to rise to approximately 3.1% in 2026, with the Iran war’s energy shock adding further upward pressure on top of the existing tariff-driven inflation. The combination of tariffs and the energy shock has raised the risk of stagflation slow growth combined with persistent high inflation.

Is there a real risk of a global recession in 2026? Yes, meaningfully higher than at the start of the year. Moody’s placed recession odds at 49% for the United States in March 2026. Goldman Sachs forecast a 30% recession risk. EY-Parthenon estimated 40%. Global GDP growth is projected to slow from 2.9% in 2025 to 2.6% in 2026. The Dallas Fed estimates that the Hormuz closure is reducing global real GDP growth by approximately 2.9 percentage points on an annualised basis during the second quarter of 2026.

What is BRICS and how is it challenging the US dollar? BRICS is an intergovernmental economic and political bloc originally comprising Brazil, Russia, India, China, and South Africa, now expanded to include Saudi Arabia, the UAE, Iran, Egypt, Ethiopia, and Indonesia representing roughly 45% of the world’s population and over 35% of global GDP. BRICS nations are building alternative financial infrastructure including BRICS Pay, mBridge (cross-border digital currency settlement), and the BRICS Unit (a gold-and-currency-backed settlement instrument launched in 2026) to reduce dependence on the US dollar and the SWIFT financial system. Russia and China now settle approximately 90% of their bilateral trade in non-dollar currencies. However, the dollar remains dominant in global transactions at approximately 89% of all foreign exchange trades as of 2025.

Why are gold prices so high and will they continue rising? Gold prices surged 55% in 2025, surpassing $4,000 per ounce for the first time in October, driven by tariff uncertainty, central bank buying, and ETF demand. J.P. Morgan forecasts prices reaching $5,000 per ounce by late 2026. Central banks globally purchased more than 1,000 tonnes of gold annually for three consecutive years more than double historical averages reflecting a broad institutional move to diversify away from dollar-denominated assets. The Iran war and the Hormuz crisis have added further momentum to gold’s safe-haven appeal.

Which countries are most vulnerable to the current global economic disruptions? The most vulnerable countries are energy-importing developing nations with high debt burdens and limited fiscal space including Pakistan, Bangladesh, Sri Lanka, Egypt, Lebanon, and multiple Sub-Saharan African nations. Europe faces a second energy crisis following the Russia-Ukraine war. Japan and South Korea are highly exposed due to their near-total dependence on Gulf oil. Iran itself is experiencing catastrophic economic conditions. UNCTAD estimates that 3.4 billion people live in countries already spending more on debt service than on health or education, making them extremely vulnerable to commodity price shocks.

Could the Strait of Hormuz crisis be resolved quickly? Potentially, but resolution depends on a ceasefire in the US-Israel-Iran conflict, which at the time of writing remains active. Iran has shown some willingness to allow passage for ships from nations it considers friendly it permitted seven Malaysian vessels through in April 2026. The US simultaneously blockading Iranian ports from April 13 creates a standoff in which both sides have economic incentives to de-escalate but also political constraints that make compromise difficult. Analysts who expect a relatively swift resolution point to Iran’s own economic need to export oil. Analysts who expect a prolonged disruption point to the political and military dynamics that make any significant concession domestically difficult for whichever government emerges from Iran’s current post-Khamenei power transition.

What could replace the US dollar as the global reserve currency? No single currency is positioned to replace the dollar in the near or medium term. The Chinese yuan faces fundamental constraints most importantly, China’s capital controls prevent the free convertibility that a reserve currency requires. BRICS nations are building parallel financial infrastructure but their internal divisions (India explicitly rejects replacing the dollar) prevent unified action. The most likely outcome, over a decade or more, is a more multipolar reserve currency system in which the dollar remains the most important but faces meaningful competition from the yuan, the euro, and potentially gold-backed digital settlement instruments. Full replacement of the dollar as the singular reserve currency, if it happens at all, is a multi-decade transition rather than an event.

How are ordinary people around the world feeling this crisis in their daily lives? The primary channels are: higher fuel and energy bills, higher food prices (driven by both energy costs and fertilizer supply disruption), higher transport costs across air and sea freight that pass through to consumer goods prices, weakening currencies in developing nations that raise the cost of all imported goods, and tighter household budgets that reduce spending on discretionary items. In the developing world, these pressures are combining with existing debt crises and food insecurity in ways that threaten basic living standards. In the developed world, the primary manifestation is a persistent squeeze on household purchasing power and political anger directed at both governments and economic institutions.

Disclosure: This article may be displayed alongside Google AdSense advertisements. All opinions, analysis, and factual information in this article represent the independent editorial judgment of the Atlas Gaming World Affairs desk and have not been influenced by any advertiser, government, political party, or external organisation. This article is provided for general informational and educational purposes. It does not constitute financial, investment, or political advice. Readers should consult qualified professionals before making any financial or investment decisions. All statistics and claims are sourced from publicly available reporting by UNCTAD, the International Energy Agency, the Dallas Federal Reserve, the World Economic Forum, J.P. Morgan Global Research, Goldman Sachs, and major journalistic institutions including Reuters, the BBC, CNN, Fortune, and Arab News. Sources were accurate at time of research but conditions are changing rapidly. AtlasGaming.com is not affiliated with any government, political party, financial institution, or advocacy organisation. All content on this page complies with Google AdSense Publisher Policies. This article does not contain hate speech, does not promote violence, does not provide investment advice, and does not contain adult content.

© 2026 AtlasGaming.com – All Rights Reserved

Table of Contents

- Helldivers 2 Ultimate Survival Guide: Best Weapons, Builds, Missions & Pro Tips (2026)

- The PlayStation 6 – Everything Gamers Have Been Waiting For – Specs, Power, Features, and the Future of PS Gaming

- Global Crisis 2026 – The New World Order? How Nations Are Reshaping Global Power and Economy- What Happens After the Dollar Era?

- The Witcher 3: Wild Hunt – The Fantasy Masterpiece That Redefined Open-World RPGs

- Diablo 4: Lord of Hatred Complete Guide – Story, Classes, Endgame & Secrets

KOORUI Gaming Monitor, 24″ IPS Monitor

| Brand | KOORUI |

| Screen Size | 23.8 Inches |

| Resolution | FHD 1080p |

| Aspect Ratio | 16:9 |

| Screen Surface Description | Flat |

Leave a Reply